Financial Engineering. Lecture 4. Option Strategies. Bullish Strategies Risk Reward Call purchase limited unlimited Synthetic long stock unlimited unlimited Bull spread limited limited Protective Put limited unlimited Bullish calendar spread limited unlimited

1.18k views • 97 slides

5th Lecture 10 th November 2003. FRAs (Swaplets) and Interest Rate Futures contracts. Forward rate agreements - exchanges of fixed rate for floating rate at a pre-determined time in the future Obviously swaps are nothing else but series of standardized FRAs

651 views • 42 slides

Business F723. Fixed Income Analysis Week 12 Credit Derivatives and Review. Credit Derivatives. Similar to the way interest rate derivatives allow the transfer of some of the interest rate risk, credit derivatives allow an investor to transfer credit risk to others

511 views • 42 slides

Intensity Based Models Advanced Methods of Risk Management Umberto Cherubini. In this lecture you will learn Extract default intensity from market data Model the dynamics of the intensity of default and the credit spread Calibrate the recovery rate from the CDS and the bond markets

512 views • 36 slides

Liquidity Risk Premia in Corporate Bond Markets. Frank de Jong Joost Driessen INQUIRE Hamburg, March 2006. Motivation. Two important puzzles in corporate bond markets Time-series variation of credit spreads Integration/segmentation of equity and corporate bond markets?

632 views • 30 slides

424 views • 28 slides

Chapter 7 (Conti.)98.10.16. Global Bond Investing. Bond Valuation. Valuation of zero coupon bonds There exists an inverse relationship between market yield and bond price. Valuation of coupon bonds. Bond Valuation. Yield to maturity: Zero coupon bonds Yield to maturity: Coupon Bonds.

419 views • 24 slides

International Securities Exchange. December 2006. Stable Market Opportunities. December 2006.

304 views • 22 slides

Corporate Financing under Ambiguity: A Utility-Free Multiple-Priors Approach. Date: 15th/November/2012 Author: C.C. Chen. Outline. Stage 1 Central issue of this study Motivation and Background Stage 2 Trick to address the central issue

309 views • 18 slides

Intensity Based Models Advanced Methods of Risk Management Umberto Cherubini. In this lecture you will learn The concept of hazard rate and of intensity Model the dynamics of intensity (Poisson, double stochastic models and Cox models) Extending the model to include positive recovery rates

181 views • 17 slides

Credit Derivatives. Chapter 29. Credit Derivatives. credit risk in non-Treasury securities developed derivative securities that provide protection against credit risk types asset swaps total return swaps credit default swaps credit spread options credit spread forwards

1.13k views • 16 slides

288 views • 15 slides

Pricing Corporate Bonds. Should Corporate Bonds be priced off the BOND CURVE or the SWAP CURVE? David Rajak, Rand Merchant Bank, IMN Conference 30 October 2007. Comparison of markets. Snapshot of SA bond market. Primary dealer system for government bonds 9 primary dealers

225 views • 12 slides

A bond is a debt instrument in which an investor loans money to the issuer for a defined period of time and receives coupons paid by the issuer at fixed interest rate. The bond principal will be returned at maturity date. Bonds are usually issued by companies, municipalities, states/provinces and countries to finance a variety of projects and activities. Fixed rate bonds generally pay higher coupons than interest rates. An investor who wants to earn a guaranteed interest rate for a specified term can choose fixed rate bonds. The benefit of a fixed rate bond is that investors know for certain how much interest rate they will earn and for how long. Due to the fixed coupon, the market value of a fixed rate bond is susceptible to fluctuation in interest rate and therefore has a significant interest rate risk. There are two types of bond valuation models in the market: yield-to-maturity model and credit spread model. This presentation gives an overview of fixed rate bonds and also elaborates two valuation models. You can more information at http://www.finpricing.com/lib/FiBond.html

135 views • 10 slides

108 views • 9 slides

Many analysts believe shale production will increase when oil tops $60 a barrel since that is the level where the wells are profitable. These analysts also believe there are a number of well heads ready to be turned on whenever prices are high. Or as an oil analyst with the Boston Consulting Group, said, “For now, the OPEC-Russia bromance continues.”

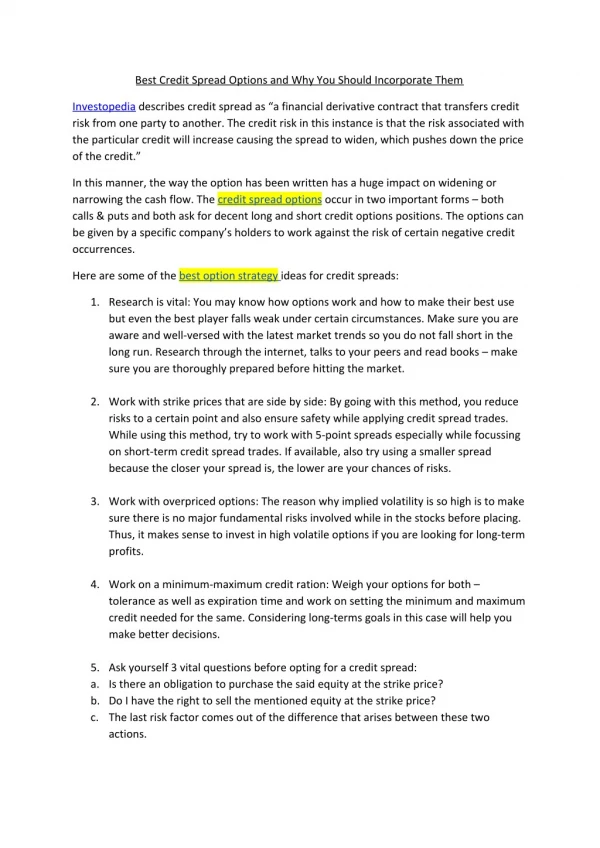

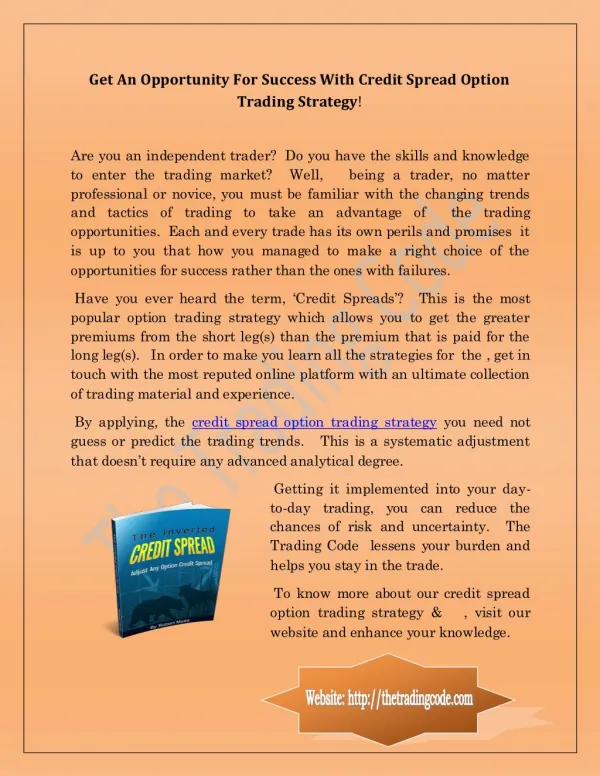

Are you an independent trader? Do you want to gain skills and knowledge to enter the trading market? Well, being a trader, no need of any professionalism in this field. You must be familiar with the changing trends and tactics of trading. Credit Spread Option Trading Strategy helps in Acquiring knowledge about Successful Trading

105 views • 1 slides

Load more. Loading.View Credit spread PowerPoint (PPT) presentations online in SlideServe. SlideServe has a very huge collection of Credit spread PowerPoint presentations. You can view or download Credit spread presentations for your school assignment or business presentation. Browse for the presentations on every topic that you want.